Do central banks drive stock returns?

/

Hat tip: Marketwatch

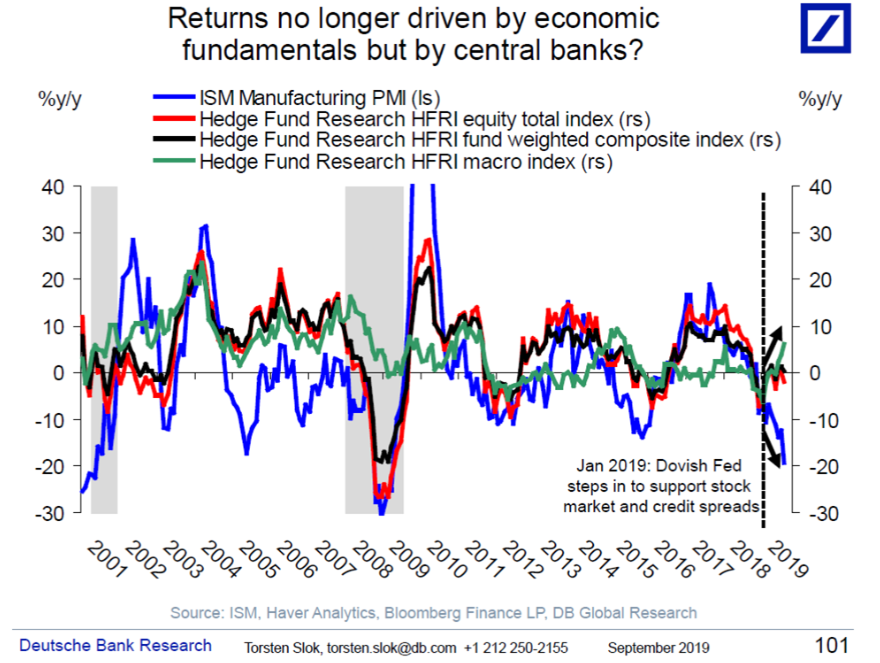

I saw some interesting reports on a Deutsche Bank report by the bank’s chief economist Thorsten Stok. His thesis is that stock market returns may no longer be driven by economic growth because Central Banks determine so much.

He points to the performance of the S&P (+17% YTD as of yesterday), despite an increasing chance of recession in the US.

Going back to basics, there are a number of reasons why stocks should perform. Key ones are:

Higher/lower future cash flows: The value of a company is the present-day value of all of its future cash flows. Those cash flows increase or decrease with economic growth, in very general terms. Obviously, some companies grow in recessions, and some companies loss money in good times, but in aggregate you should see earnings move in line with economic growth. And as the chance of a recession increases, expectations about future cash flows should fall, and stock prices should follow.

Source: Vietecon.com

Discount rate: But as I as said, the stock price is the present value of future cash flows. The present value is determined by the discount rate. The discount rate is the risk free rate plus a market risk premium multiplied by the Beta of the stock, or its volatility in relation to the market. Basically, cash flows are discounted by an amount that is higher than the risk-free rate, because everyone could get that. Say by investing in US government bonds.

So there are three things there that have a big impact: risk-free rate, the market risk premium and the Beta. This is all part of the capital assets pricing model (CAPM).

As we can see in the chart to the right, a change in the discount rate affects value a lot. Let’s assume a company that makes $10 a year for 25 years and then shuts down. It could be worth $250 if cash flows are not discounted, or $100 if the discount rate is 10%. To follow this all the way down, if have a discount rate of 100%, the company would be worth just $10 - the amount that could be taken out the first year.

Side note: In terms of sausage making, if you are an equity analyst and want to change the valuation without changing a lot of numbers, there are a number of easy ways to do it: change the discount rate by raising/lowering the beta, the target debt percentage, or the free cash flow in the final year, since so much of valuation is in the terminal value.

Demand: There is a third way that stocks are priced. And this one is maybe not as powerful as the other two. Basically the stock market is like any other market. Demand and supply matter a lot. Demand can change for a few reasons. Maybe more people are investing in stocks because they are looking for better returns than what they can find in the bank and/or because they are saving more. Central banks may actually step in and buy stocks. Or countries, say one of the big sovereign wealth funds, may decide to allocate more to stocks and/or have more money generally for some reason.

One of the hardest thing for me to answer when I was an equity analyst is this: who is going to be the marginal buyer for the stock? This question speaks to demand, and I didn’t always have a good answer. It could be anyone! But for the market as a whole, because I was looking at emerging and frontier markets, it mostly was investors allocating more to the asset class of emerging market stocks.

Back to the Slok’s article. Here’s what Slok thinks is driving the market:

"Perhaps the answer is that equity and credit markets are no longer driven by fundamentals, but instead by Fed and ECB promises of lower rates, more dovish forward guidance, and QEternity."

"In short, because of unlimited central bank safety nets — including in the new MMT form of aggressive fiscal policy — S&P500 may not decline, and credit spreads may not widen next time we enter a recession."

It doesn’t really seem correct to say that markets aren’t driven be fundamentals . His statements point to a few fundamentals of valuation:

Lower future discount rates (because central banks are holding down the “risk-free rate”)

Maybe some idea that recessions will be shorter or less bad, so that cash flows won’t fall as much.

Potential demand from the central banks or from qualitative easing keeps demand high for stocks.

Lower rates making bond yields look less attractive compared to stock returns.

What I don’t know is if stock prices will perform well in a true recession. I think it will depend on how bad the recession is. Basically, does falling cash flows offset a lower discount rate and demand from the government/QE?